Law Of Supply And Market Equilibrium

The law of supply is a fundamental principle of economic theory that states that an increase in price leads to an increase in quantity supplied when all other factors remain constant. In other words, price and quantity have a direct relationship: quantities respond in the same direction as price changes. This means that, in order to increase profits, producers are willing to offer more of a product for sale on the market at higher prices by increasing production.

An entire supply curve can shift right or left due to changes in production costs and related factors. As a result, at a given price, a higher or lower quantity is supplied. Prices and quantities supplied are related by supply curves if no other factors change. The ceteris paribus assumption is what it's called.

Shifts in the Supply Curve

A supply curve depicts how quantity supplied changes as price changes, assuming ceteris paribus—no other economically significant factors change. If other supply-related factors change, the entire supply curve will shift. A change in supply entails a change in the quantity available at each price point.

Let's say we have an initial supply curve for a specific type of vehicle. Consider what happens if the price of steel, an important component in car manufacturing, rises, increasing the cost of producing a car.

The supply curve shifts to the left, toward S1, as a result of higher manufacturing costs. Firms will profit less per car, so they will be motivated to produce fewer cars at a given price, reducing the number of cars available.

Cost reductions would have the opposite effect, shifting the supply curve to the right, toward S2. Firms would profit more per car, motivating them to produce more cars at a given price, thereby increasing the quantity supplied.

OTHER FACTORS THAT AFFECT SUPPLY

We saw in the previous example how changes in the prices of inputs in the manufacturing process affect the cost of production and, as a result, the supply. The cost of production is also influenced by a number of other factors.

1. Natural conditions

The Manchurian Plain in northeastern China, which produces the majority of China's wheat, corn, and soybeans, recently experienced its worst drought in 50 years. Drought reduces agricultural product supply, implying that at any given price, a smaller quantity will be supplied. Good weather, on the other hand, would shift the supply curve to the right.

2. New technology

The supply curve will shift to the right when a company discovers a new technology that allows it to produce at a lower cost. In the 1960s, for example, a major scientific effort known as the Green Revolution focused on breeding improved seeds for basic crops such as wheat and rice. By the early 1990s, these Green Revolution seeds had been used to grow more than two-thirds of the wheat and rice grown in low-income countries around the world, with harvests twice as high per acre. A technological advancement that lowers production costs will shift supply to the right, allowing for more production at any given price.

3. Government policies

Taxes, regulations, and subsidies can all have an impact on the cost of production and the supply curve. Businesses consider taxes to be costs. For the reasons stated above, higher costs reduce supply. Another example of cost-affecting policy is the plethora of government regulations that require businesses to spend money in order to provide a cleaner environment or a safer workplace; following regulations raises costs.

On the other hand, a government subsidy is the polar opposite of a tax. When the government pays a company directly or reduces the company's taxes in exchange for certain actions, this is known as a subsidy. Taxes or regulations, from the perspective of the firm, are an additional cost of production that shifts the supply curve to the left, causing the firm to produce fewer units at each price. Government subsidies, on the other hand, lower production costs and increase supply at all prices, shifting supply to the right.

WHAT IS MARKET EQUILIBRIUM?

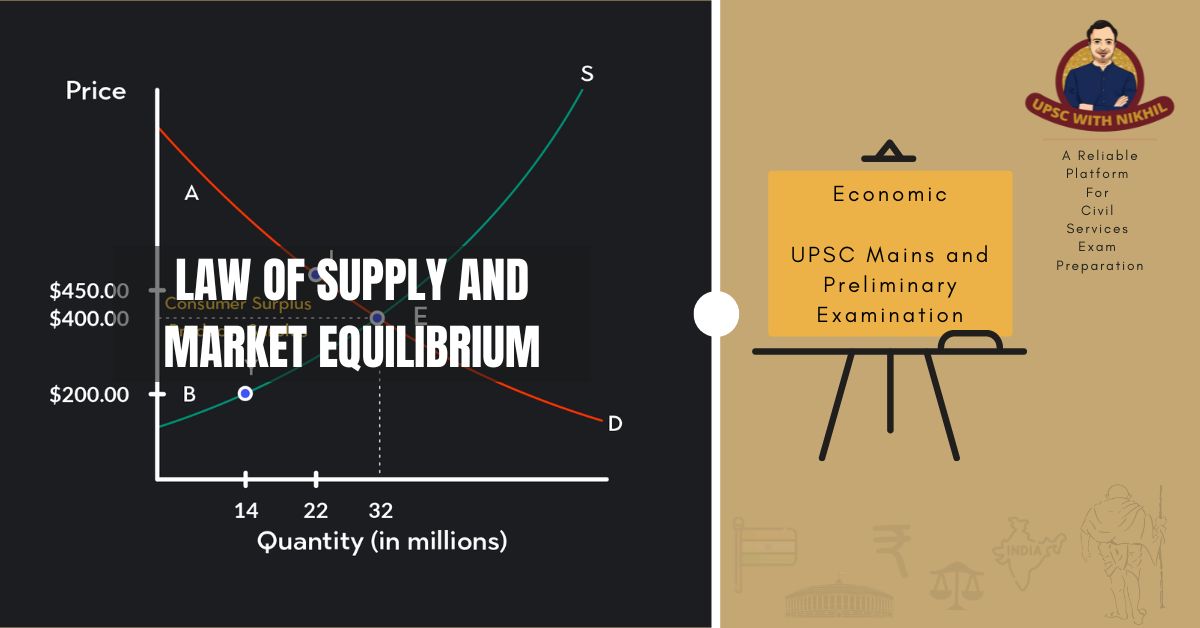

Economic equilibrium is a state in which economic forces such as supply and demand are balanced and the (equilibrium) values of economic variables do not change in the absence of external influences. In this case, market equilibrium refers to a situation in which a market price is established through competition such that the quantity of goods or services sought by buyers is equal to the quantity produced by sellers. The competitive price, also known as the market clearing price, is a price that does not change unless demand or supply changes, and the quantity is referred to as the "competitive quantity" or market clearing quantity.

At the equilibrium price, the supply and demand curves cross. This is the price at which the market will be able to function.

Because the price on the vertical axis and quantity on the horizontal axis of demand and supply curve graphs are the same, the demand and supply curves for a particular good or service can appear on the same graph. Demand and supply work together to determine the price and quantity of goods bought and sold in a market.

The equilibrium point E is where the demand curve, D, and the supply curve, S, intersect, with an equilibrium price of 1.4 dollars and an equilibrium quantity of 600. The equilibrium price is the only one at which the quantity demanded and supplied are equal. There is excess supply at a price above equilibrium, such as 1.8 dollars, because the quantity supplied exceeds the quantity demanded. Quantity demanded exceeds quantity supplied at a price below equilibrium, such as 1.2 dollars, resulting in excess demand.

The equilibrium price is the only price at which consumers' and producers' plans coincide—that is, when the quantity consumers want to buy of a product, quantity demanded, equals the quantity producers want to sell, quantity supplied. The equilibrium quantity is the name given to this common quantity. The quantity demanded does not equal the quantity supplied at any other price, so the market is not in equilibrium.

The term "equilibrium" refers to a state of balance. There is no reason for a market to move away from its equilibrium price and quantity if it is at its equilibrium price and quantity. If a market is not in equilibrium, however, economic pressures emerge to move the market toward the equilibrium price and quantity.